The energy system powers every corner of the modern economy from oil for transport and chemicals, to natural gas for heating and industry, to coal for electricity generation and steel production. Oil and gas provide over 50% of world primary energy which rises to over 80% when including coal, forming the backbone of global supply today and highlighting the magnitude of the task of an energy system transformation. This system keeps the world moving and powers economic activity, but it is prone to geopolitical disruption and price volatility. This volatility has highlighted long-term concerns that Calvert has long held about the extent to which the current global energy system relies on fossil fuels.

Energy crises have knock-on effects on living standards and require significant financial support to shield populations from the negative ramifications. These concerns are in addition to the role the energy sector plays in climate change. The energy industry is inextricably linked to the issue and together global oil & gas production and use contribute over 50% of global fossil-related greenhouse gas emissions. Their long-term use needs to be drastically cut to limit the most destructive impacts of climate change.

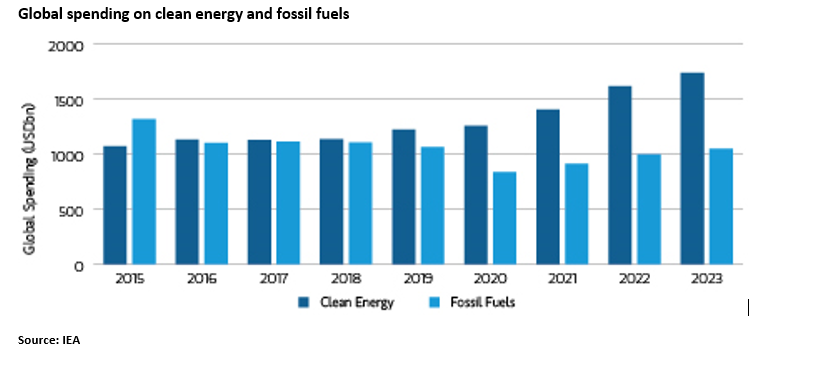

The energy system is changing to address some of these concerns, but there is no consensus on the pace or shape of the transition. We think some are factoring in too much change too quickly, while others are expecting too little to happen too slowly. Renewable energy in its various forms has exerted the highest growth in the last two decades, increasing in scale as rapidly falling costs have made these technologies cost competitive with fossil fuels. As a result, deployment levels are growing at an exponential rate - global renewable installations (in GWs) roughly doubled from 2018-2022 and are set to increase approximately 30% year-over-year in 2023. Since 2018, on an aggregate level, cleaner form of energy generation and use attract more capital than traditional fossil fuels, a trend we think with continue going forward.

However, barriers to broader deployment in the short term are emerging - cost pressures, supply chain disruption, higher raw material costs, and higher interest rates among others. Additionally, the electricity grids need to evolve to accommodate these technologies along with better battery technology and the permitting of new projects needs to be streamlined. As the energy transition unfolds, fossil fuels will continue to play an important role in the global system. As our Chairman John Streur has said, "I don't mind the narrative that everything is going to be running on wind and solar soon, but I doubt the narrative is right. There's too much at stake and it's too early to say if that's the way things are going to work. It's a fascinating question and it involves everything from chemistry and physics to geopolitics and economics."1

Impacts for responsible investors

Uncertainty about the energy sector's medium-to-long term future lies in how increasing direct competition between traditional fossil fuel sources and renewables plays out in the coming years and decades. We believe that with each passing year the world will get closer to reaching peak oil demand, meaning that the energy sector will go 'ex-growth' in the next decade. Whilst still subject to large uncertainties, the prospect of falling global fossil fuel demand post 2030 will place strains on the traditional energy corporate business models. We also think that while oil and gas demand will remain substantial for years to come, the overall direction of incremental economic opportunities from global decarbonisation (and associated additional earnings streams) in coming decades will largely fall outside of the sector's core activities.

Against this backdrop, Calvert looks to influence the energy industry by:

- Deploying capital more effectively to energy-consuming companies in other sectors that are deploying clean energy technology to decarbonize, and in doing so cutting fossil fuel demand.

- Maintaining a forward-looking approach in our investment decisions and understand that change in the sector is gradual and that oil & gas will feature in the energy system for many years to come. We seek to avoid solely basing judgements on companies' current emissions and focus on companies that are successfully changing with the energy transition and therefore may benefit from economic opportunities that emerge from the process.

- Encourage the oil and gas industry to decarbonize its own operations. Oil & gas production is a large emitter and there are actionable steps that companies can take in an economically beneficial manner.

The good news is that companies in the sector are making positive changes and we have seen broad-based efforts by the industry to cut operational emissions, engage more meaningfully on ESG topics in general and scale back 'growth at all costs' strategies. The scale of these changes is creating meaningful differentiation in how companies are approaching the energy transition and allows us to identify certain oil and gas companies that are actively changing with energy system and meet Calvert's Principles for Responsible Investment.

To read more about Calvert's approach to the energy transition, click here.

Bottom line: The decarbonization journey presents opportunities for responsible investors in the energy sector as companies both evolve their strategies and take differentiated approaches to manage the energy transition. We don't see producing oil and gas today and investing in the energy transition as mutually exclusive, but we are selective over which energy companies we feel meet the Calvert Principles. During this next decade we hope to see energy companies proactively evolve with the energy transition by diversifying and broadening their businesses to align with wider decarbonization trends, undertake material investment in the energy transition, and curtail growth in long-term fossil fuel production.