"Everywhere in India there are anecdotal but important signs of growing aspirations."

Insights

No capex, no cry

Featured

All Articles ()

There are currently no articles for this filter

KEY POINTS

1. India's standout growth story is garnering increased attention among emerging markets investors.

2. Optimistic households are borrowing more, causing some concern over the build-up of "China-like" debt risks.

3. While higher private capex would help boost economic activity, the current growth trend appears stable and offers potential upside for fixed income investors.

Boston - On a recent research trip to India, we arrived with two key questions: First, should rising household debt be a concern? And second, where is the private capex? Concerns over household debt relate to China's current debt-induced malaise. The fear among many Indians is that "We will be like China," if policymakers don't address rising debt now.

For private capex, without higher investment the government's own 7% growth forecast seems to us unrealistic. If that growth rate goes unrealized, some argue that India might never converge to the major powers with which it intends to compete.

Hopeful households borrowing more

Thankfully, neither concern looks likely to derail the current India story, with household debt being the easier and simpler of the two to dismiss. Everywhere in India there are anecdotal but important signs of growing aspirations; people are upgrading homes, investing their savings and generally looking for self-advancement.

Notably, sidewalk bookstores are full of self-improvement books. Indian households, at least in the geographies and economic segments currently prospering, are in a virtuous circle wherein increased motivation feeds off and into rising economic opportunity. It is not a stretch to assume that many Indians reasonably expect higher future income and feel comfortable borrowing against that.

Concerned about capex?

The "missing" capex question is trickier. India's future would be brighter, if private capex were stronger. That said, current growth rates are sustainable and consistent with gradual convergence to higher income rivals.

How is this possible?

First, public capex is strong and this is not "bridges to nowhere." The capital stock in India is so low, and therefore the returns on capital so high, that even the less efficient public sector can develop economically beneficial projects.

Prime Minister Narendra Modi's is itself casting off the common image of inefficient government in India; the legend has it that Modi officials work 18-hour days. "Inspiration" is best found by the private sector, but in today's India the public sector does plenty of "perspiration."

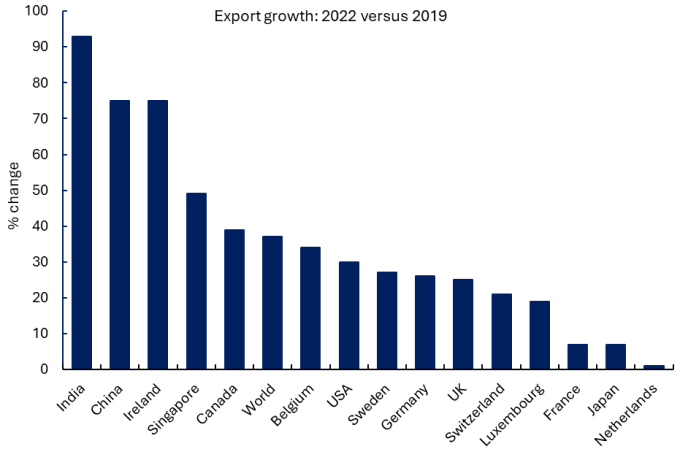

The second mitigant is that the current growth drivers in India are capex-lite. Specifically, the underappreciated story of India is the boom in service exports. India's software developers require much less upfront investment than its factory workers. But the benefits to the macroeconomy from their labor are largely the same.

India leads in global exports of digitally delivered services

Source: "What Drives India's Services Exports?" RBI Bulletin, p.188, April 2024; Authors use data from WTO Trade Outlook, April 2023.

For illustrative purposes only. Past performance is no guarantee of future results.

The country's legion of IT services workers generates foreign exchange, which keeps the value of the rupee stable. The stable rupee allows for stable interest rates, which the government borrows at for stable funding of the capex push. This growth formula vaguely mirrors the successful development of Korea and Taiwan. It's too early to say it will work over the long term, but there are no immediate holes in the playbook.

Rate outlook

Against the current backdrop, could surprises be in store for rates? Here, we do not foresee a hike. Remember, if there's no private capex boom around the corner, and if households are not in a state of irrational exuberance, the risk that the Reserve Bank of India (RBI) needs to hike lessens.

Meanwhile, the stable rupee would allow RBI to cut should circumstances warrant, like a global downturn. If policy rates won't rise but they might fall, the market should be pricing a downward bias for rates, which would translate into potential upside for India's fixed income investors.

Bottom line: Right now, investors generally seem enamored with India. On balance, growth looks sustainable while concerns over household debt and limited private capex appear overdone. The stable rupee should limit scope for a negative surprise on rates, which makes India attractive for fixed income investors today.