The urgent need to reduce emissions has recently drawn a high level of scrutiny and interest from the financial services sector. Although physical climate risk is often mentioned less than transition risk, its effects will become increasingly evident over time. The insurance industry offers an important perspective on the evolving materiality of physical risk and ways to address it.

Property insurance helps society recoup the economic losses associated with natural disasters. As such, re/insurance companies that offer property coverage play a critical role in enabling economies and populations to adapt to accelerating climate change. As responsible investors, our exposure to this industry is relevant for two reasons. First, it provides us with valuable insights into how, where, and when physical climate risk is manifesting itself in financially material ways. Second, it gives us the opportunity to allocate capital to help address the societal challenges stemming from changing weather patterns.

Economic Costs Rise Along with Natural Disasters

Over the last 20 years, the number of global natural disasters has increased from approximately 340 to 400 in 2023. The frequency of these events has increased in every world region; but in the U.S. this has being particularly pronounced with the number of natural disasters almost doubling - from about 50 in the early 2000s to almost 100 in the last few years.1

This trend has had negative impacts both across the global economy and within the insurance industry. Aggregate insured losses for the industry rose from $26 billion in 2000 to $118 billion in 2023 and reached well over $100 billion in six of the last ten years.2

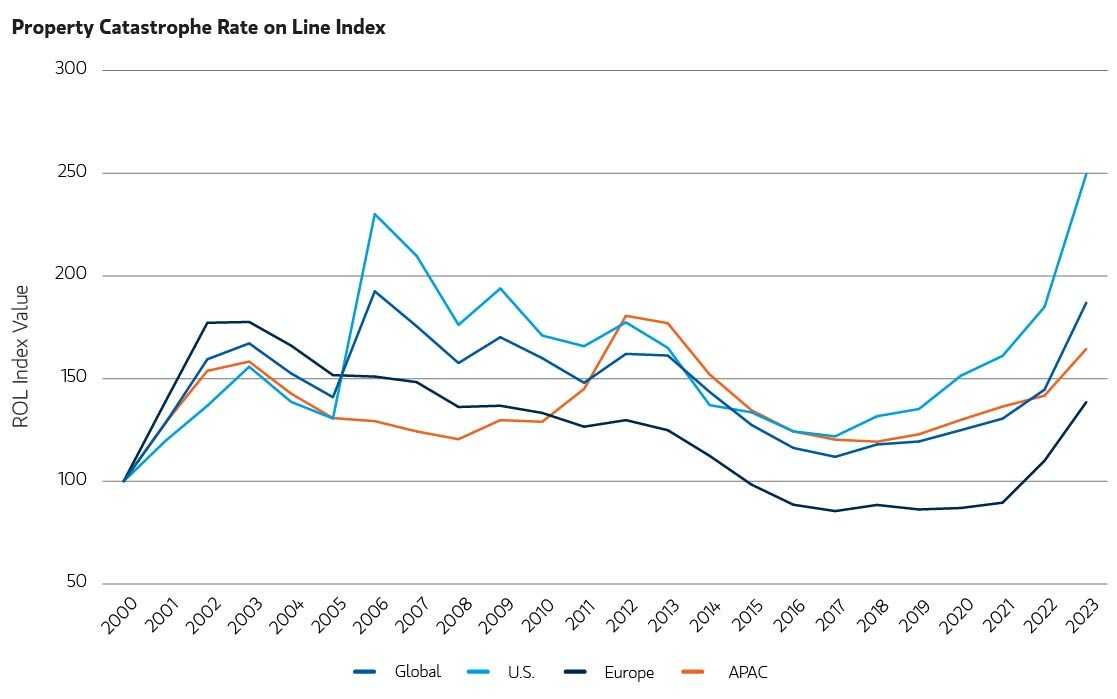

Rocketing Costs of Catastrophe Coverage

To navigate this environment, the re/insurance industry has leveraged the demand from investors for high, uncorrelated returns to tap opportunities in the catastrophe bond market.3 Since 2000, nominal issuances of property catastrophe bonds increased almost twentyfold, reaching $15 billion in 2023.4 This has helped diversify and expand the pool of capital to mitigate physical climate risk, beyond the organic capacity of the industry players themselves. However, the influx of external capital has not been sufficient to offset the depletion in reserves driven by the rising frequency and severity of climate disasters, and the recent surge in global inflation.

These conditions have ignited an unprecedented acceleration in the price of catastrophe coverage in the reinsurance market. Property catastrophe reinsurance rates increased over 29% globally in 2023, up for six consecutive years. In the U.S., this dynamic is particularly acute, with rates doubling from 2017 to 2023, reaching their highest level ever.5

In view of these factors, we believe that:

- North America is increasingly vulnerable to changing weather patterns. Calvert's exposure to re/insurers operating in this region allows us to partner with firms that we believe stand to benefit the most from our regular dialogue as responsible shareholder. Nonetheless, we are aware of the investment downside associated with physical climate risk. Therefore, we favor issuers that provide transparent and detailed disclosures about: i) their track record in mitigating this risk; ii) their property exposures to high-risk areas; and iii) their strategy to remain profitable while supporting societal adaptation to climate change.

- Although the inverse relationship between volumes and prices is an intrinsic and recurring feature of insurance cycles - and therefore, it is fair to expect a reversal of this dynamic - climate change is not likely to be mean-reverting in the medium term. Therefore, while maintaining a balanced exposure across the industry, we believe that reinsurers are better positioned than primary insurers to capitalize on this trend. This is rooted in their ability to act as price makers if changing weather patterns continue to affect the profitability of the property segment, and insurance capital remains scarce.

Bottom line: The insurance industry provides valuable insights into the impacts of climate change. North America appears increasingly vulnerable to changing weather patterns, presenting significant opportunities for responsible investors, as well as some risk. We seek to mitigate the risks by requiring strong disclosures and strategic positioning from the re/insurance companies we invest in. At a higher level, we believe that climate change is an issue that will likely lead to a recurring scarcity of insurance capital available to cover property risks. Against this backdrop, reinsurers appear to have a structural advantage relative to primary insurers.